Imagine a life without any debt payments weighing you down – no student loans, car payments, or credit card bills. Picture having an additional $300, $500, or even $800 in your monthly budget. This is the debt-free life you’ve been dreaming of, and the most efficient way to turn this dream into a reality is through the debt snowball method.

Understanding the Debt Snowball Method

The debt snowball method is a strategic approach to reducing debt. It involves paying off your debts in ascending order of size, regardless of their interest rates. Beyond its rapid debt-reducing effects, the debt snowball method is designed to transform your financial behavior, preventing you from falling back into debt.

Here’s how the debt snowball method works:

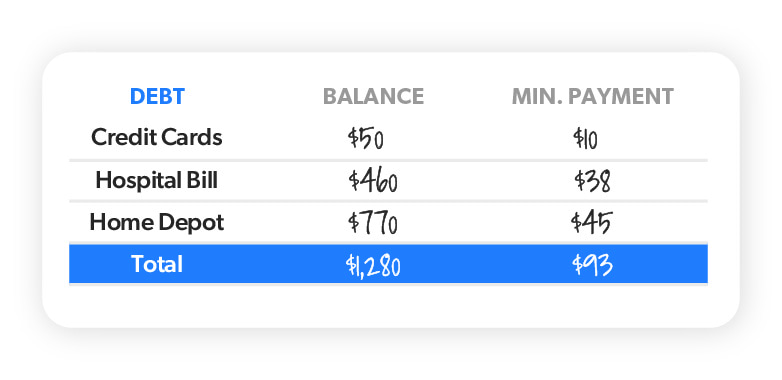

Step 1: Arrange your debts from smallest to largest.

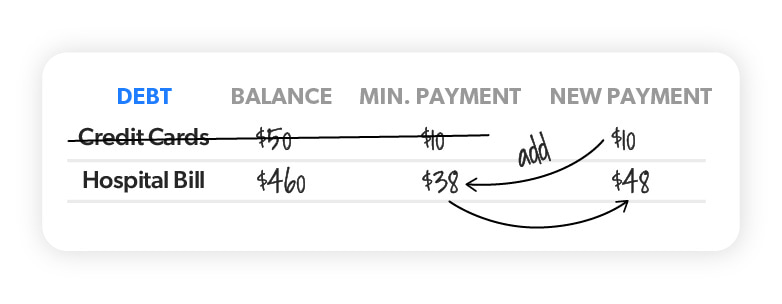

Step 2: Make minimum payments on all debts except the smallest. Direct as much money as possible toward that smallest debt. Once it’s paid off, take the payment you were making on it and apply it to the next smallest debt. Continue paying the minimum on other debts.

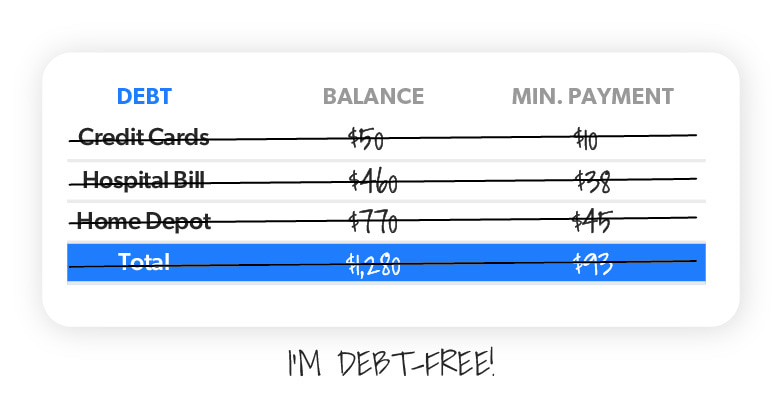

Step 3: Repeat this process as you work through your debts. As you eliminate each debt, the amount you can contribute to the next one increases, akin to a snowball gaining momentum as it rolls downhill.

The Psychology Behind Ignoring Interest Rates

Although it might seem logical to prioritize high-interest debts first (known as the debt avalanche method), personal finance is largely about behavior, with knowledge playing a smaller role. While the debt avalanche might make sense mathematically, it might not be as effective in practice. Beginning with the smallest debt provides quick wins that motivate you to continue, unlike the larger debts that could stall your progress and lead to frustration.

The debt snowball leverages these quick wins, building momentum and motivation from the outset. Our experience in guiding people to financial freedom has shown that the debt snowball is the most effective and swiftest route to becoming debt-free.

What to Include in Your Debt Snowball

Your debt snowball should encompass all non-mortgage debts, which includes anything you owe to others. Examples of such debts are:

- Student loans

- Medical bills

- Car loans

- Credit card balances

- Home equity loans

- Personal loans

- Payday loans

Keep in mind that while your mortgage is a type of debt, it’s not addressed until after you’ve paid off your non-mortgage debts and established an emergency fund equivalent to 3–6 months’ worth of expenses.

When to Start Your Debt Snowball

Commence your debt snowball journey once you’ve set aside a $1,000 starter emergency fund. While this fund may not cover all emergencies, it provides a buffer for minor unexpected expenses, allowing you to focus on the debt snowball.

Ready to Begin? Let’s Roll!

Are you prepared to take the plunge into your debt snowball journey? Start by listing your non-mortgage debts, then factor in your monthly household income. You can also accelerate your progress by adding an extra monthly payment to your debt snowball. If your debt-free date seems distant, there are various strategies you can try:

- Develop a budget to optimize your money allocation.

- Increase your income through side gigs or other means.

- Sell unused items to boost your debt repayment funds.

- Cut down on expenses to redirect more income to your debt snowball.

- Consider enrolling in Financial Peace University for comprehensive financial education.

With a solid plan in hand, the time for action has arrived. Transition from dreaming about a debt-free life to actively creating it. Start your debt snowball today and watch your financial freedom gain momentum!

Leave a comment